ICOLI (insurance company owned life insurance) is a life insurance program used as a corporate financing tool with tax and capital efficiency benefits.

These structures align with long-term liability-driven strategies, enable diversification across private market asset classes and have the potential to strengthen balance sheets. However, insurers face several considerations when implementing an ICOLI program. Strong governance, effective risk management and alignment with liability needs are critical.

StepStone offers purchasers of ICOLI access to what we consider high-quality private market investment strategies to optimize risk, returns and liquidity.

Introduction

The shift toward private markets

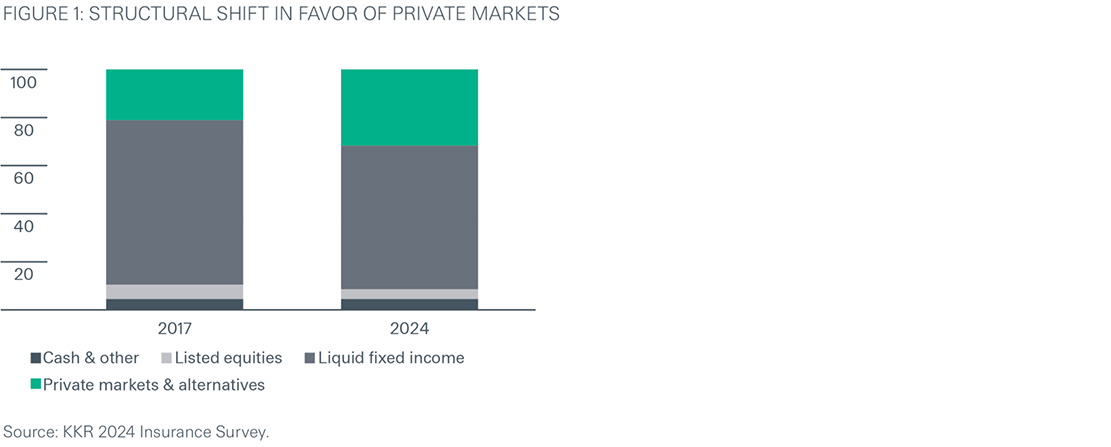

Driven by a variety of factors, insurers have increased their allocations to private markets (Figure 1).

- Facing low interest rates and bond yield compression in recent years, insurers have added private market exposures (especially private debt) to complement public fixed-income investments that they’ve long relied upon.

- Inflationary, demographic and supply/demand pressures are further compelling insurers to allocate more toward “total return” strategies including private equity, real estate and infrastructure equity, which offer capital appreciation and income.

- That insurers are required to consider asset liability matching (ALM) in their investment selections is another reason for the shift toward these private market strategies that are intrinsically long-term by nature.

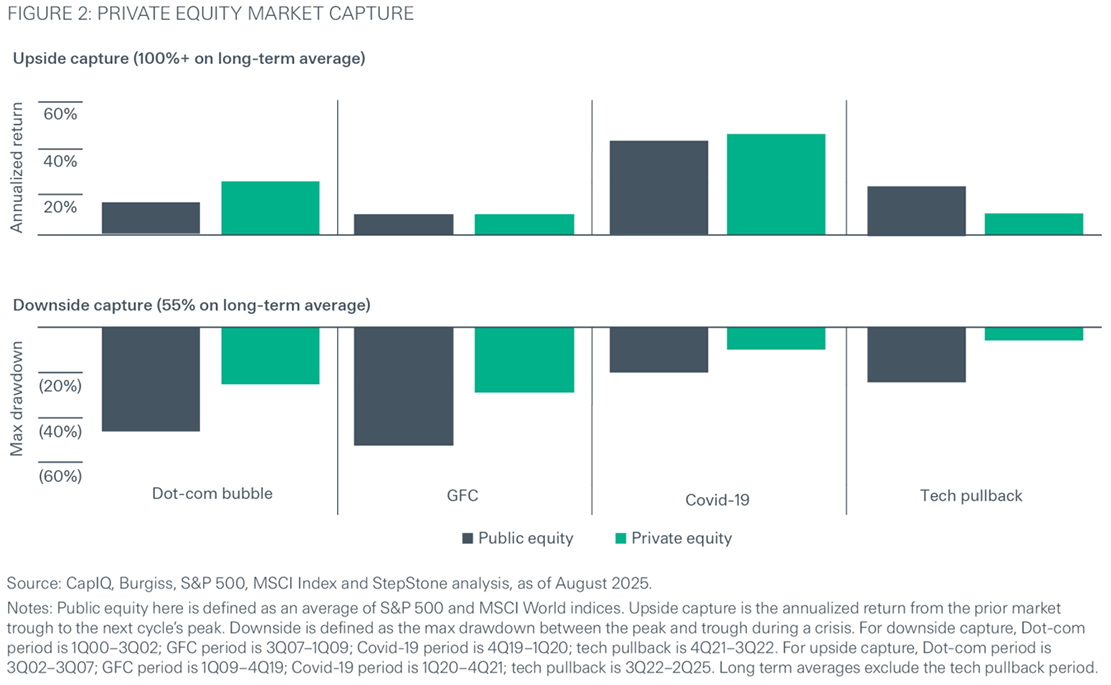

- Market volatility, traditional public market asset correlation and geopolitical risks present additional reasons why insurance investors are looking toward diversifiers that can provide downside protection without compromising upside potential—something private equity has been able to achieve over the long run (Figure 2).

Recent surveys suggest this strategic shift isn’t fleeting: Most insurers plan to increase their allocations to private markets over the next two years.1

While private markets can solve the myriad needs of insurers (i.e., income, capital appreciation and diversification), they introduce challenges such as liquidity management and complex investment structures. Moreover, certain regulatory regimes impose higher risk-based capital (RBC) charges on private market assets.² These factors require insurers to balance return objectives with operational considerations. As such, tax efficiency and capital optimization have become critical in evaluating private market allocations.

Innovative structures

To optimize long-dated liabilities and investment allocations, some insurers have turned to purchasing insurance company owned life insurance (ICOLI) and using insurance dedicated funds (IDFs).

- ICOLI is a life insurance policy used to insure the lives of a select group of consenting executives, serving as a flexible funding mechanism for employee and executive benefits and balance sheet management. The insurance company is the policy owner, premium payor and beneficiary of the policies while senior employees are the insureds. The investment returns of the funds held in the policy can accumulate to the insurance company on an income tax-free basis so long as the assets are not surrendered.

- IDFs are specialized investment vehicles designed to hold assets within an insurance-compliant structure (like an ICOLI). Today’s IDFs can provide customized access to private markets.

ICOLI benefits

ICOLI may offer compelling financial advantages. When properly structured, the policy owners may achieve enhanced after-tax returns with lower capital requirements, supporting long-term, liability-driven strategies. With policy durations of 20 to 40+ years, ICOLI enables tax efficient capital compounding over long periods. For example, a $100 million allocation compounding at 8% over 20 years grows to $466 million, avoiding approximately $76.9 million in taxes at a 21% corporate rate.

By providing a tax-advantaged income stream, ICOLI may deliver operational benefits, including enhancing net income and mitigating key-person risk for insurers. The policy is recorded as an asset on the insurer’s balance sheet for as long as the covered employees remain alive, and its tax-exempt investment returns improves overall financial performance. In the event of an insured executive’s death, the insurer receives income tax-free death benefit proceeds. These proceeds can help offset lost revenue, cover recruitment and replacement costs and mitigate the financial impact of the loss.

Beyond tax and operational benefits, ICOLI can have attractive capital treatment under the NAIC and rating agency models. Capital charges are 0–5% depending on regulatory classification (0% for health and life insurance companies; 5% for property and casualty insurers) and the credit quality of the issuing life insurer.³ The result is an attractive return profile for RBC charge.⁴

Structural alignment

By partnering with a private market specialist, insurers can access off-the-shelf or customized IDFs to sit inside their ICOLI.

- The first thing to consider is asset allocation: Do you prefer public assets, private assets or a combination? Within private markets, which sectors are most suitable: Private equity, private debt, real estate or infrastructure? The answer may depend on the insurer’s objective—whether to optimize income, capital appreciation, or both through total- return metrics.

- Second is structure: Do you want the instant deployment and continuous exposure that evergreen funds offer? Or are the customization and flexibility inherent to a separately managed account or closed-ended funds a better fit? There are trade-offs either way, and IDFs can be designed to meet the needs and objectives of each insurer.

- Asset managers with IDF products can add further value if they have the scale and expertise to offer secondaries and co-investments alongside primary fund commitments. Secondaries offer shorter durations and enhanced distributions, whereas co-investments can reduce the overall fee-load of the IDF.

Risks and challenges

Insurers face several considerations when implementing an ICOLI program. Strong governance, effective risk management, and alignment with liability needs are critical.

- Illiquidity risk: Private market assets are often long term and illiquid, with lock-up periods exceeding 10 years, especially when structured in drawdown vehicles. While ICOLI policies span 20 to 40 years or longer, insurers must ensure liquidity for claims and liabilities is not compromised.

- Structural complexity: ICOLI is a customized life insurance contract, requiring specialized administration, compliance oversight and robust governance to avoid operational or regulatory missteps, which could jeopardize any tax and capital efficiency benefits. Additionally, IDFs must comply with specific diversification requirements and adhere to investor control limitations to remain compliant.

- Tax considerations: Although ICOLI offers tax-deferred growth and favorable accounting treatment, improper structuring and utilization can lead to unintended consequences.

- Regulatory and capital uncertainty: Favorable RBC treatment is a key advantage, but interpretations under NAIC and/or rating agencies may evolve. Insurers must also monitor counterparty risk; a downgrade of the issuing insurance carrier could affect capital efficiency.

- Usage: Because ICOLI is designed to offset a specific executive benefit liability, there is likely a limitation to how much ICOLI the insurer can (or should) purchase.

Conclusion

ICOLI has the potential to offer insurers a powerful combination of tax-deferred growth, capital efficiency, and alignment with liability-driven objectives. With experienced IDF providers and third-party administrators delivering diversification and governance, ICOLI stands out as a strategic enabler for private market allocations and potentially enhanced risk-adjusted returns.

1 KKR 2024 Insurance Survey, SLC Management Global Insurance Group 2025 Insurance Asset Management Survey and BlackRock 2025 Global

Insurance Report: Opportunity Amid Uncertainty.

² The NAIC applies high RBC charges for private fund investments for US-based insurers.

³ Typically large, well-capitalized carriers with A or higher ratings.

⁴ There’s a wealth of information on the benefits and mechanics of ICOLI. See for example An introductory guide to iCOLI by Mezrah Consulting.

Want a copy of this paper?