Given the extensive media attention on direct lending in recent months, we believe it is important to clarify several of the most frequently highlighted issues.

Much of the current commentary risks conflating different segments of the credit market and, in doing so, blurs the distinctions between segments of the asset class. This has contributed to a degree of confusion among investors. The purpose of this paper is to provide context, address common misconceptions, and distinguish between headline risk and the recent developments in the direct lending market.

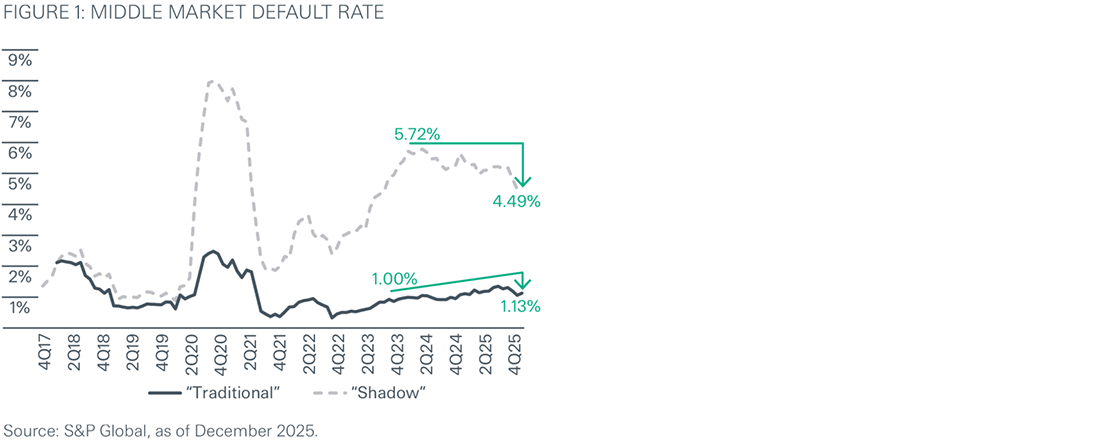

The “shadow” default rate

Headlines increasingly mention the “shadow” default rate within direct lending as proof of growing default risk within the asset class. However, the term is somewhat of a misnomer: PIK interest payments, maturity extensions, covenant waivers, and other amendments are all lumped together as part of the shadow. While signs of potential stress, these situations do not represent actual defaults. Rather they are proactive measures taken to address temporary underperformance or liquidity pressure and to stabilize borrowers. Nonetheless, some may regard the shadow default rate as an omen of future defaults. To date, though, there is limited evidence to support this claim.

Payment defaults have risen slightly from the unusually low levels seen in 2022, when government support programs during Covid helped keep defaults down. However, the overall increase remains modest. Importantly, it is materially smaller than the recent decline in the reported shadow default rate (Figure 1). This suggests that the tools commonly used by private lenders, such as amendments, extensions, or PIK, have, in several cases, helped borrowers stabilize and avoid costly bankruptcy proceedings. Although some companies ultimately defaulted, the available evidence indicates that most have not.

In addition, several of the more widely publicized payment defaults have been incorrectly associated with direct lending, as many of the affected borrowers actually fall outside the traditional scope of the strategy. A significant number of these cases relate to large-cap issuers normally found in the broadly syndicated loan market and are not representative of the middle-market companies typically found in direct lending portfolios. Others involve asset-based lending structures rather than cash flow-based direct lending, reflecting a fundamentally different underwriting approach and risk profile. Furthermore, a number of these situations concern non-sponsored borrowers, which represent a relatively small and more niche segment of the direct lending market. Taken together, these factors highlight that many of the recent high-profile defaults are not indicative of broad-based stress within the sponsored middle-market direct lending space but instead reflect dynamics specific to adjacent or less representative segments of the market.

Overall, we expect payment defaults to increase in the coming quarters. But we view this as a normalization from the exceptionally low post-Covid levels, rather than an early sign of broader stress within the direct lending market, which continues to benefit from a constructive macroeconomic environment.

Payment-in-kind

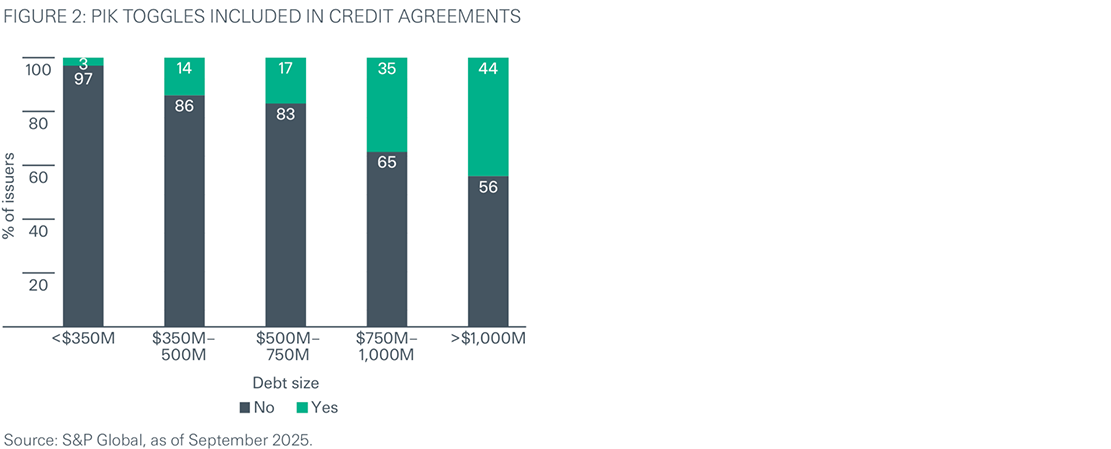

Recent media coverage, often in connection with the so-called shadow default rate, has highlighted the perceived risks associated with PIK interest payments in direct lending. Borrower-friendly conditions continue to characterize the current market, as strong fundraising cycles have increased available capital while also creating deployment pressure for managers, contributing to the inclusion of features such as PIK toggles in certain transactions.

Importantly, these provisions are not applied uniformly across the market (Figure 2). PIK optionality remains primarily concentrated among larger, more established issuers and is generally not available to smaller or more highly leveraged borrowers. In those instances, lenders tend to maintain tighter structural protections and stronger cash-pay requirements. In many cases, borrowers seeking this level of flexibility have traditionally accessed the broadly syndicated loan or high-yield bond markets, where documentation standards are typically more permissive than in direct lending. As competition for larger transactions has increased, private managers have at times needed to align certain terms, such as covenants, with those available in public markets. In addition, they also offer targeted flexibility, for instance in the form of a PIK toggle, to remain competitive and justify the higher spreads asked by private lenders.

We also note that PIK optionality is not costless. Electing to PIK interest typically increases the spread, compensating lenders for the additional risk and discouraging indiscriminate use by borrowers. Available evidence suggests that only a small proportion of companies with PIK optionality in their loan documentation actually use it, indicating that its presence does not necessarily translate into widespread utilization.

That said, PIK is generally not an attractive feature for private lenders, especially when it results from a loan amendment (often referred to as “bad PIK”). Even a PIK structured at origination (“good PIK”) can hurt recovery rates, as it defers cash flows toward maturity and increases overall credit risk.

Valuations

The press has raised concerns about valuations within direct lending portfolios, citing the asset class’s relative opacity, the absence of regular secondary market trading, and perceived conflicts of interests related to managers’ fee incentives. As a result, the valuation process has come under increased scrutiny, with some commentators suggesting that reported values may not adjust quickly enough to reflect underlying credit deterioration.

However, direct lending valuations fundamentally differ from public market pricing. Unlike traded instruments, which can reflect short-term market sentiment and liquidity conditions, direct lending loans are valued primarily through fundamental credit analysis, focusing on the borrower’s financial performance and expected repayment prospects. Consequently, valuations tend to reflect long-term economic value rather than short-term market volatility.

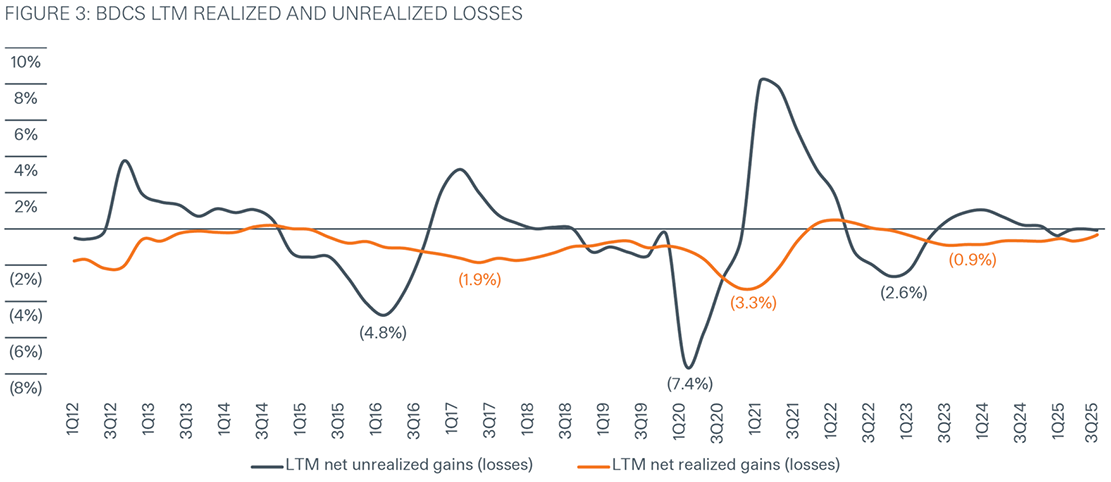

Historical experience also suggests that valuation practices in direct lending have generally been conservative: During periods of financial stress, cumulative markdowns have typically exceeded realized losses by approximately 1.7–2.5x, indicating a prudent approach to credit risk (Figure 3). While some degree of subjectivity is inherent in any illiquid asset class, material discrepancies appear to be uncommon and are usually concentrated in distressed or highly idiosyncratic situations.

Recent instances of significant price discovery that affected the NAV of certain BDCs were largely driven by developments at a limited number of individual borrowers. These cases reflect borrower-specific events rather than evidence of systemic valuation issues across the direct lending market.

In addition, BDC valuation processes are typically complemented by independent third-party valuation providers. These experts review key assumptions and credit developments to help ensure that portfolio valuations are fair, consistent, and aligned with industry standards and regulatory expectations.

BDC redemptions

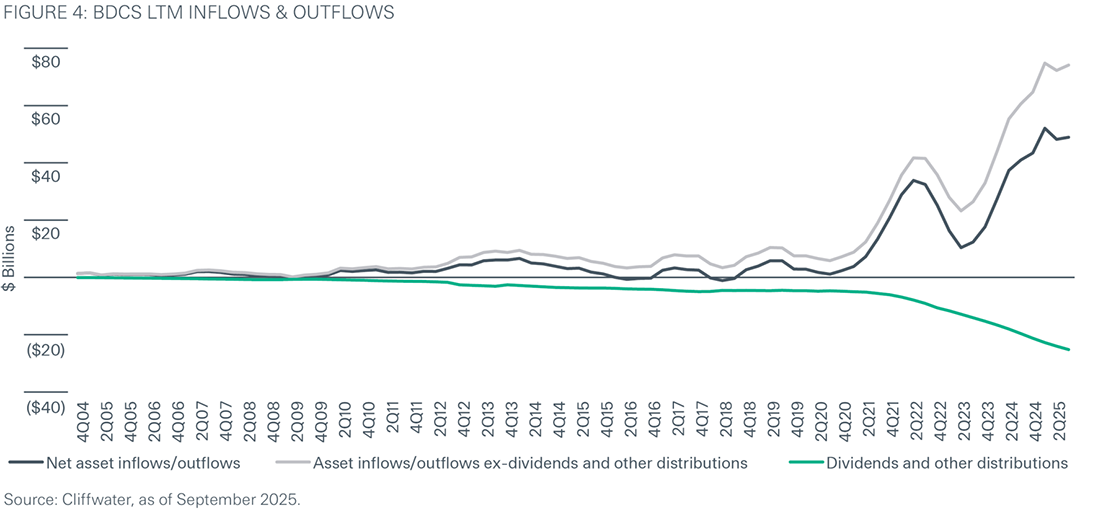

Media coverage has increasingly focused on elevated redemption activity in certain BDCs in recent quarters, often presenting these outflows as a sign of stress. But this view captures only part of the picture. While redemption requests have increased in some vehicles, most BDCs continue to report positive net flows overall, supported by ongoing investor demand and new subscriptions.

Importantly, most redemption requests have been met in full—at times exceeding the typical quarterly threshold of 5% of NAV. Several managers have demonstrated their ability to accommodate higher redemption levels without resorting to forced sales of private assets or materially impacting portfolio performance. In this sense, recent activity can be viewed as a real-time stress test of the BDC model, providing evidence that liquidity is being managed actively and prudently within the constraints of the semi-liquid structure.

It is also notable that the highest redemption levels have been concentrated in products primarily distributed to individual investors and, in certain cases, associated with weaker relative performance or lower portfolio quality. This dynamic has contributed to widening dispersion across managers, with stronger-performing products and established portfolios experiencing more stable flows and, in some cases, benefiting from relative inflows.

At the same time, some commentary has cited declining dividend levels as evidence of deteriorating asset quality. In practice, the moderation in distributions largely reflects lower base interest rates and tighter credit spreads. As rates decline, the floating-rate income generated by portfolios naturally decreases (Figure 4). This dynamic does not alone indicate a material increase in defaults or realized credit losses within underlying portfolios.

AI & software

AI has the potential to reshape certain industries or business models. While this is not a new observation, renewed investor focus on AI-driven growth expectations contributed to a sharp correction in segments of the public technology sector. More recently, volatility in tech equities has prompted concerns that a potential slowdown in AI-related spending could spill over into direct lending portfolios.

It is important to emphasize that such risks are not unique to direct lending. Any meaningful correction in AI investment would likely transmit through broader macroeconomic and credit channels, rather than the asset class itself.

Private debt investors have financed some of the recent build-out of AI infrastructure and computing capacity through asset-backed facilities rather than traditional direct lending structures. As a result, much of this activity sits outside the scope of direct lending. Within traditional direct lending portfolios, most middle-market companies may be more likely to purchase AI-enabled services or computing capacity than build proprietary infrastructure. In this context, a growing supply of computing resources could ultimately reduce costs and enhance operating efficiency through automation and productivity gains. Conversely, a sharp slowdown in AI investment would likely affect broader economic growth and credit conditions across all markets

Within the software sector, the rapid evolution of AI is expected to produce disruptions and differentiated outcomes among issuers. Some companies may benefit from enhanced efficiency and new product capabilities, while others —particularly certain SaaS providers—may face pressure if customers develop in-house solutions using more accessible AI tools. Although software exposure exists within some direct lending and venture debt portfolios, structural protections help mitigate risk. Direct lenders typically hold senior secured first-lien positions and aim to maintain loan-to-value (LTV) ratios below 50%, providing a meaningful equity cushion.

In this environment, concentration risk is more relevant than sector exposure alone. As outcomes within software are likely to be uneven, diversification across industries, sub-sectors, and individual borrowers remains a key risk-management tool. A prudent direct lending approach therefore includes limiting exposure to more volatile technology segments and recurring-revenue (ARR-based) structures, prioritizing senior secured first-lien positions, and avoiding excessive single-name or single-sector concentrations.

Direct lending market in general

Direct lending in 2025 was characterized by resilient fundraising, tight lending terms, and continued deployment pressure amid subdued M&A activity. Capital raising remained solid, supported by a recovery in European fundraising and strong growth in evergreen structures. At the same time, the resulting capital overhang reinforced a competitive, borrower-friendly environment and drove further compression in gross spreads.

Deal volumes remained within historical ranges, although activity was initially skewed toward refinancings, add-on acquisitions, and dividend recapitalizations, reflecting the slower pace of private equity exits. More recently, transaction data suggests a gradual pick-up in M&A activity, which could help rebalance supply and demand dynamics through higher deal flow in 2026.

While returns moderated from the strong levels seen in 2024, performance remained resilient. The decline was primarily driven by lower base rates and tighter spreads rather than credit losses. Importantly, gross asset yields remain above long-term historical averages and are expected to remain supportive into 2026. Base rates, while easing, are still elevated relative to the past decade, spreads appear to be stabilizing, and a recovery in transaction activity could even create scope for modest spread widening in the year ahead.

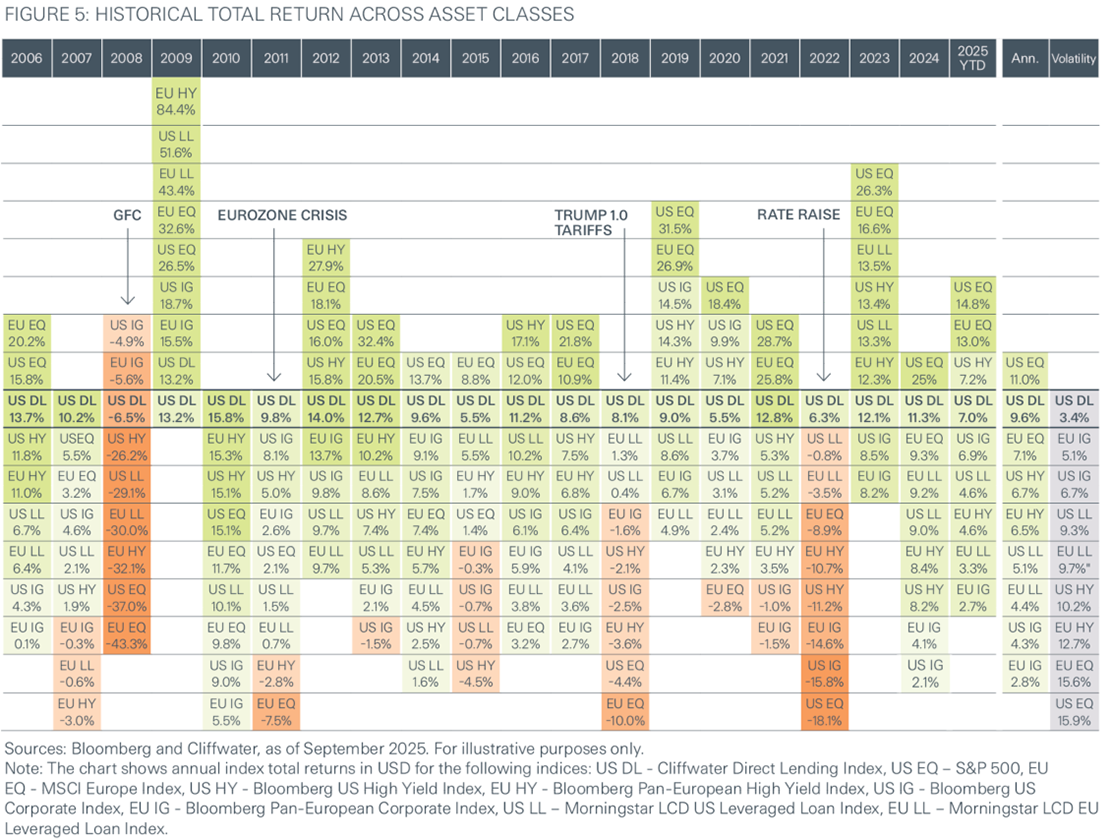

Underlying credit fundamentals have also improved incrementally. Leverage levels and LTV ratios remain contained, interest coverage metrics are recovering, and default rates, while higher than the unusually low levels observed in 2022, remain manageable and below long-term averages. In a public market environment where equity valuations appear stretched and spreads in leveraged loans and high-yield bonds have tightened significantly, direct lending continues to offer attractive relative value. As the market enters 2026, the asset class appears well positioned to deliver stable and compelling risk-adjusted returns, supported by elevated income levels, gradually improving borrower fundamentals, and a broadly benign default environment (Figure 5).

Conclusion

Recent headlines have amplified concerns around direct lending, but much of the narrative reflects selective data points, a conflating of different credit segments, or a misunderstanding of how the asset class functions. All of this has contributed to unnecessary confusion for investors. A closer examination suggests that many of the highlighted risks are either idiosyncratic or already well understood and managed within established underwriting and portfolio construction frameworks.

At the same time, underlying fundamentals remain sound. Default rates are normalizing from unusually low levels, valuation practices remain disciplined, and liquidity management within semi-liquid vehicles has demonstrated resilience.

As the market enters 2026, direct lending continues to offer attractive all-in yields relative to public credit. While a more competitive environment and selective pockets of risk warrant continued discipline, the asset class remains well-positioned to deliver stable income and compelling risk-adjusted returns. For long-term investors, success in direct lending continues to hinge on disciplined underwriting, careful asset selection, and broad diversification—combined with active management of fees and expenses.